What is a Double Trigger mechanism, how does it work in an exit, and what should you know about its tax implications?

For many high-tech companies, an employee option plan is one of the most important compensation tools. It allows employees to share in the company’s success, while helping the company strengthen employee commitment over time.

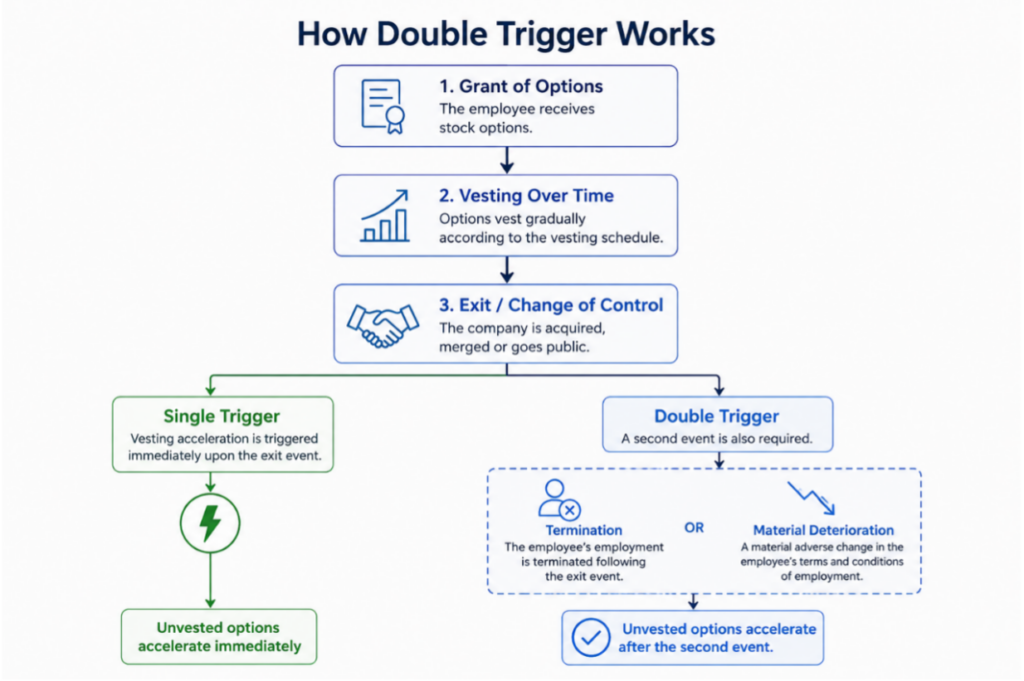

When an acquisition, merger, or change of control occurs, the question arises as to how the transaction will affect options that have not yet vested. To address these situations, many option plans include a mechanism known as a Double Trigger.

This mechanism is not limited to the relationship between the company and the employee. In certain cases, it may also affect the tax treatment of the options, particularly where the options were granted under the capital gains track of Section 102 of the Israeli Income Tax Ordinance.

In this article, we explain what a Double Trigger mechanism is, how it works, how it differs from a Single Trigger mechanism, and why it is important to review it from a tax perspective as well

What Is a Double Trigger Mechanism

In most option plans, the employee does not receive all of the options on the grant date. Instead, a vesting period is set, during which the options become exercisable gradually, as long as the employee continues to work for the company.

Sometimes, during the vesting period, a significant event occurs, such as an acquisition of the company, a merger, or a change of control. In these situations, the question arises whether the vesting period should continue as usual, or whether the employee should be able to benefit from options that have not yet vested.

For this purpose, option plans may include acceleration mechanisms. One of the most common of these is the Double Trigger mechanism.

Under this mechanism, vesting acceleration does not occur automatically upon the acquisition transaction. It is triggered only after two cumulative conditions, which were determined in advance in the option plan, are met.

In most cases, these two events are:

- A change of control in the company, such as an exit, merger, or acquisition.

- After completion of the transaction – termination of the employee’s employment or a material adverse change in the employee’s employment terms, in accordance with the definitions set out in the option plan.

As long as both conditions have not been met together, the options will continue to vest in accordance with the original schedule.

How Does the Mechanism Work in Practice?

This can be illustrated with a simple example.

An employee received 8,000 options, which are scheduled to vest over four years

After two years, half of the options have vested, while the other half has not yet vested.

At this stage, the company is acquired by an international company.

If the option plan includes a Double Trigger mechanism, the acquisition of the company by itself does not change the status of the options that have not yet vested.

Only if, after completion of the transaction, the employee is terminated, or if another condition set in advance in the option plan is met (for example, a material adverse change in the employee’s employment terms), the vesting acceleration mechanism will be triggered. The options that have not yet vested may then vest immediately, in whole or in part, depending on the plan.

By contrast, if the employee continues to work for the acquiring company on the same terms, the vesting period will generally continue as usual.

Single Trigger Compared with Double Trigger

There are two main mechanisms for accelerating the vesting of options: Single Trigger and Double Trigger.

Under a Single Trigger mechanism, a single event is sufficient – usually an exit, merger, or change of control – to accelerate the vesting of the options. In other words, completion of the transaction itself may cause the unvested options to vest, even if the employee continues to work for the acquiring company.

By contrast, a Double Trigger mechanism requires two cumulative conditions. The transaction alone is not enough. Vesting will be accelerated only if the second condition set out in the option plan is also met, such as termination of the employee’s employment or a material adverse change in the employee’s employment terms.

Single Trigger vs. Double Trigger

Comparison Criterion | Single Trigger | Double Trigger |

How many conditions are required? | One | Two cumulative conditions |

First trigger | Exit / merger / change of control | Exit / merger / change of control |

Second trigger | None | Usually termination or a material adverse change in employment terms |

Does an exit accelerate vesting? | Generally yes | No |

If the employee continues working for the acquirer | The options may vest immediately | Vesting generally continues according to the original schedule |

Main purpose | To provide the employee with immediate acceleration | To balance employee protection with employee retention after the transaction |

Why Do Companies Choose a Double Trigger Mechanism?

It may seem that a Single Trigger mechanism is more favorable to employees, because it allows them to benefit from the options earlier.

In practice, however, most acquisition transactions are not carried out with the intention of shutting down the company’s operations, but rather of continuing to operate the company as part of the acquiring group. In many cases, one of the key assets the acquirer seeks to acquire is the employee team.

From the acquirer’s perspective, automatic acceleration of all options on the transaction date may harm employees’ incentive to continue working for the company after the acquisition. If all options vest immediately, some employees may prefer to leave shortly after the transaction is completed.

On the other hand, employees also seek to protect themselves. Without an appropriate mechanism, an employee may find themselves terminated shortly after the exit, while a significant portion of their options has not yet vested.

A Double Trigger mechanism seeks to balance these two interests. On the one hand, it allows the acquirer to retain the employee team and continue the company’s operations. On the other hand, it provides employees with protection if the transaction ultimately results in termination of their employment or a significant adverse change in their employment terms.

For this reason, in recent years this mechanism has become one of the most common mechanisms in option plans of high-tech companies.

What Is the Connection Between Double Trigger and Section 102?

In many high-tech companies, employee options are granted under the capital gains track of Section 102 of the Israeli Income Tax Ordinance. Subject to compliance with the conditions of the law, this track enables employees to benefit from a significant tax advantage upon exercise of the options. When the options vest in accordance with the schedule set in advance in the option plan, there is generally no special difficulty from the perspective of Section 102.

The complexity begins when vesting is accelerated following an acquisition or merger transaction.

In these situations, the question arises whether the options that vested earlier than planned still meet the conditions of Section 102, or whether the acceleration itself changes their tax treatment. The distinction between taxation under Section 102 and taxation as employment income may have a significant impact on the amount of tax ultimately paid.

How Does the Israel Tax Authority Treat a Double Trigger Mechanism?

In March 2025, the Israel Tax Authority published a professional position paper addressing the accelerated vesting of options in acquisition, merger, and initial public offering (IPO) transactions.

The main message arising from the paper is that a Double Trigger mechanism, when determined in advance as part of the option plan, does not in itself impair the tax benefit under Section 102.

However, this does not mean that every case of vesting acceleration will automatically enjoy the same tax result. The Israel Tax Authority emphasizes that the full circumstances of the transaction must be examined, including the structure of the option plan, the manner in which the acceleration mechanism is applied, the type of consideration received by the employee, and the connection between termination of employment and the acquisition transaction.

In other words, the mere existence of a Double Trigger provision in the option plan is not enough. It is important to understand how it was drafted and how it is implemented in practice.

Why Does the Type of Consideration Matter?

One of the key distinctions discussed by the authority is between cases in which the employee receives consideration in shares or options of the acquiring company, and cases in which the employee receives cash consideration.

Where the options are exchanged for options or shares of the acquiring company, and they remain subject to the vesting mechanism and the terms set out in the plan, the Israel Tax Authority views this, in appropriate cases, as a continuation of the original compensation plan. By contrast, where the employee receives cash consideration, it is necessary to examine whether this is in fact a payment reflecting compensation for the employee’s work. In certain circumstances, part of the consideration may be classified as employment income rather than a capital gain, and may be taxed at a much higher marginal tax rate.

What Should Be Reviewed Before an Acquisition Transaction?

In many cases, the option plan is drafted years before negotiations for the sale of the company begin. Precisely for that reason, it is advisable to review its provisions at the early stages of the transaction.

Among other things, it is advisable to review:

- Whether the option plan includes a Single Trigger or Double Trigger mechanism.

- Whether the acceleration mechanism was determined in advance as part of the grant terms.

- The precise conditions for triggering the acceleration mechanism.

- Whether the consideration to employees will be paid in cash, shares, or a combination of both.

- Whether the transaction structure may affect the application of Section 102.

- Whether there are additional tax aspects that should be taken into account in the transaction.

In conclusion, the Double Trigger mechanism has become an integral part of many option plans in high-tech companies, mainly because it creates a balance between the needs of the company and the acquirer and the protection of employees.

However, alongside the contractual and business aspects, it is also important to examine the tax implications of the mechanism. The manner in which the option plan is drafted, the transaction structure, and the type of consideration paid to employees may affect the tax treatment and the application of the benefits provided under Section 102.

Therefore, when planning an option plan or advising on an acquisition transaction, it is advisable to examine the issue from a tax perspective as well, and not to rely solely on a legal or commercial review

Nimrod Yaron & Co. specializes in Israeli and international taxation. The firm’s team combines many years of experience at the Israel Tax Authority, leading firms, and law firms, and brings a broad legal, accounting, and economic perspective.

The firm advises private and public companies, Israeli and foreign companies, global venture capital funds, and clients seeking focused and clear advice on complex tax matters. In addition, we work with a professional network of accounting firms and law firms around the world, in order to provide comprehensive support in cross-border matters as well.

With respect to employee option plans, exit transactions, and the tax implications under Section 102, an early review of the plan structure and the transaction terms may help identify tax risks, reduce uncertainty, and prepare properly for engagement with the Israel Tax Authority.

FAQ

What Is a Double Trigger in Employee Options?

A mechanism for accelerating the vesting of options, which is triggered only when two conditions determined in advance are met. These are usually a change of control in the company followed by termination of the employee’s employment or a material adverse change in the employee’s employment terms.

What Is the Difference Between Single Trigger and Double Trigger?

Single Trigger requires only one event, such as the sale of the company. Double Trigger requires an additional event beyond the transaction, and therefore vesting acceleration does not occur automatically.

Does a Double Trigger Mechanism Impair the Tax Benefit Under Section 102?

Not necessarily. When the mechanism is determined in advance as part of the option plan, its mere existence does not deny the tax benefit. However, the circumstances of the transaction, the type of consideration, and the manner in which the plan is implemented must be examined.

Does Every Option Plan Include a Double Trigger Mechanism?

No. Some plans include a Single Trigger mechanism, some include a Double Trigger mechanism, and some do not include any vesting acceleration mechanism at all.